What is Money, Actually?

Issue No. 2 — We’ve been using a broken definition for so long we forgot the real one.

Ask someone what money is and they will describe whatever happens to be in their wallet. Dollars. Pounds. A number on a screen. They will tell you money is what the government says it is, or what people agree to accept, or what the central bank prints. These are descriptions of the current arrangement. They are not a definition of money.

This distinction matters more than almost anything in economics. Because if you define money by what currently exists, you have no framework for evaluating whether it is working. You cannot diagnose a problem you cannot name.

So let us start from first principles.

Three Jobs. One Standard.

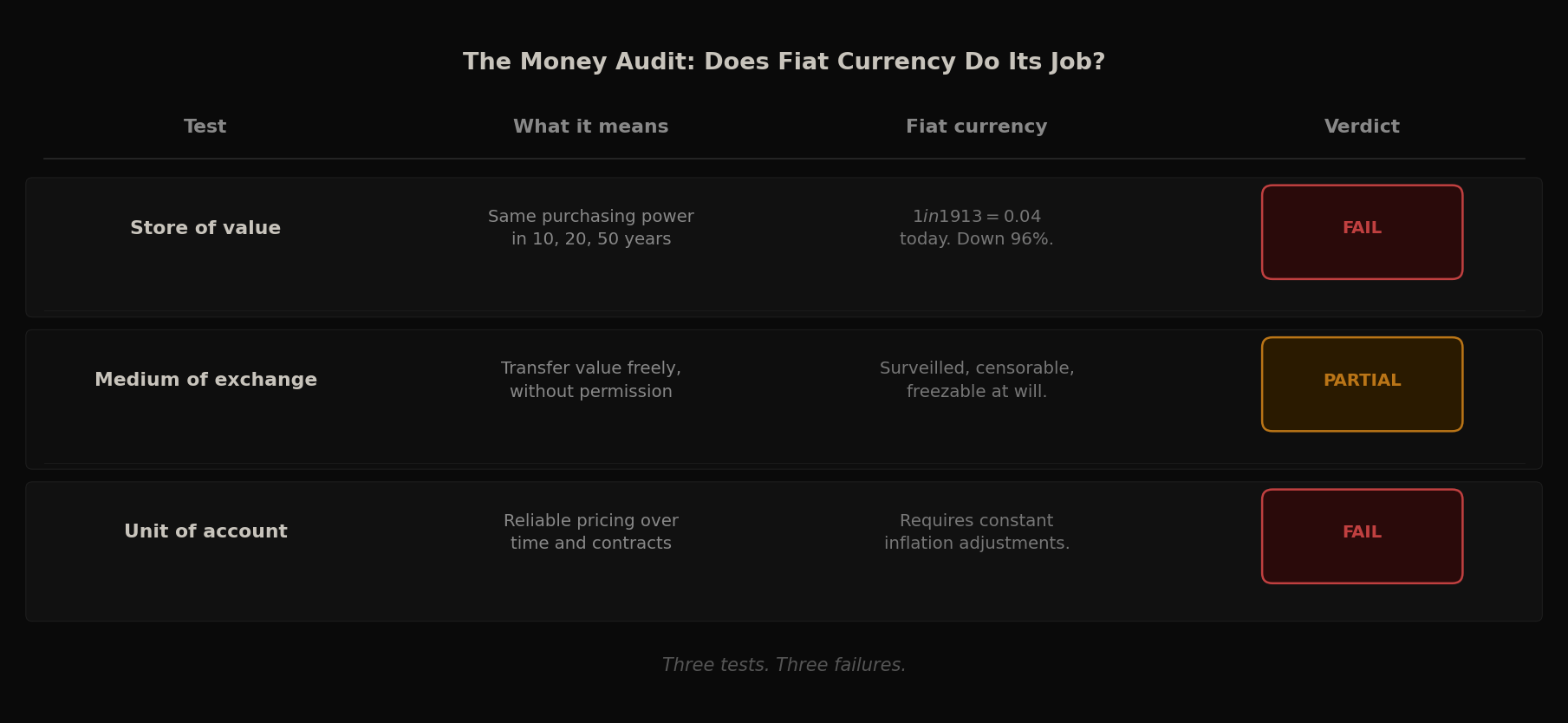

Money has three jobs. It has always had three jobs. Every monetary system in history has been evaluated against the same three criteria, whether the people using it knew the criteria or not.

The first job is store of value. Can you put money away today and retrieve the same purchasing power in the future? Not next week. Not next month. Across years. Across decades. Across generations. A good store of value means that work performed today translates reliably into consumption tomorrow. It means savings are not a race against time.

The second job is medium of exchange. Can you use money to buy things without friction? Without a middleman extracting a percentage. Without a counterparty needing to trust your identity. Without a third party having the power to block the transaction. A good medium of exchange moves value between willing parties as cleanly and directly as possible.

The third job is unit of account. Can you price things reliably in this money over time? Can you write a ten year contract, plan a retirement, or build a business model around a number that actually means something consistent? A good unit of account is stable enough to reason about the future.

Three jobs. The question is whether anything currently in circulation actually does them.

Running the Audit

Let us be honest about the dollar. Or the pound. Or the euro. Or any fiat currency issued by any government in the last century.

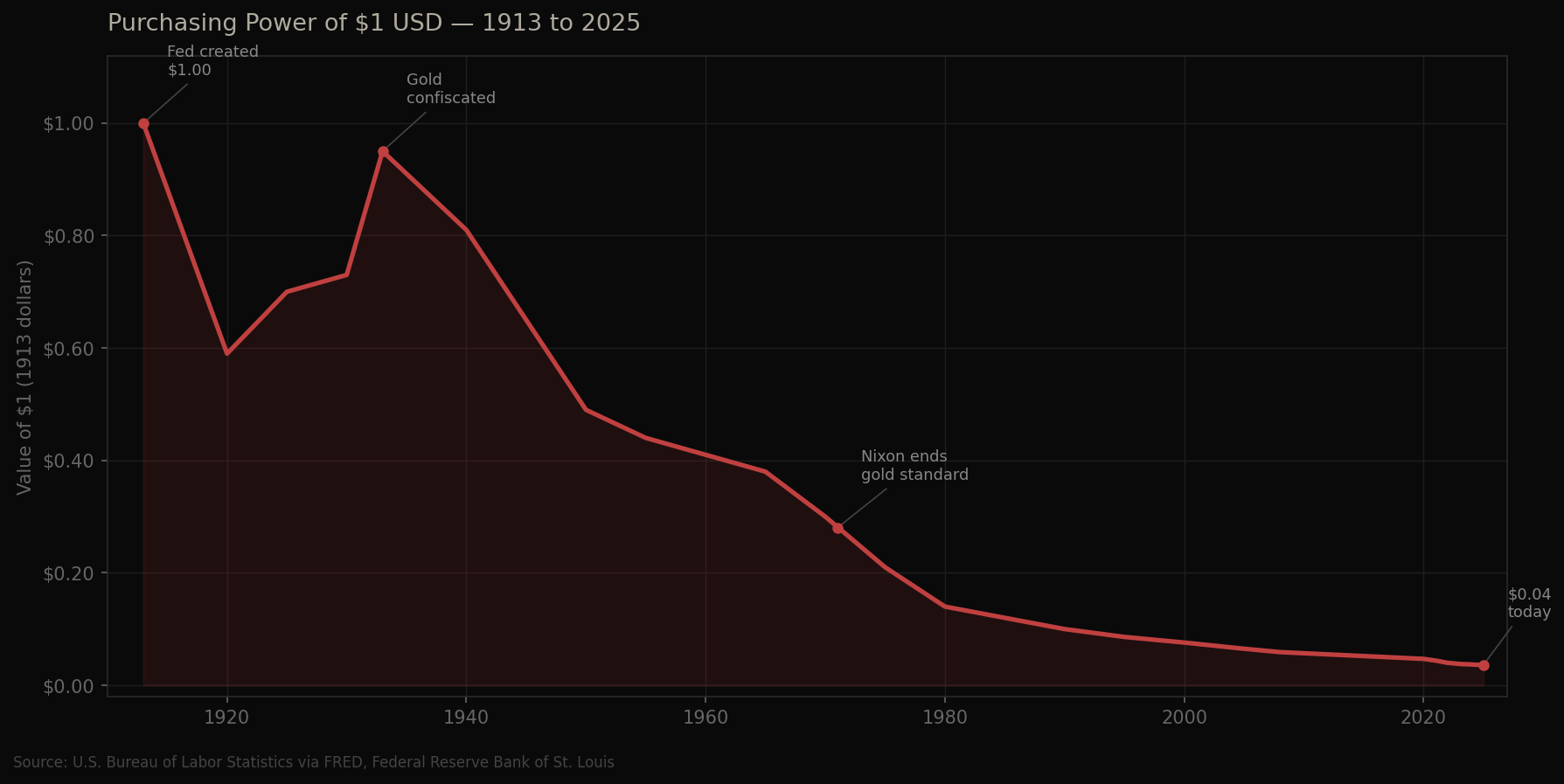

Store of value. The United States dollar has lost over 96 percent of its purchasing power since 1913. A dollar saved in 1913 buys four cents worth of goods today.

This is not a bug, it's the feature. It is the intended design of a system that requires continuous expansion to service its debts. Every fiat currency in history has followed the same trajectory. Some faster, some slower. None have preserved purchasing power across generations. The store of value test fails completely.

Medium of exchange. Technically, yes, you can use fiat currency to buy things. But the friction is higher than it appears. Every transaction is surveilled. Accounts can be frozen. Entire countries can be cut off from the global financial system with a bureaucratic signature. Payment processors can deplatform businesses. Banks can debank individuals without explanation. The medium of exchange works smoothly until it doesn’t, and the conditions under which it stops working are controlled entirely by third parties you have no relationship with and no recourse against.

Unit of account. This is the most insidious failure because it is the hardest to see. We price everything in dollars and so we think we understand what things cost. But a house that was worth $100,000 in 1990 and is worth $800,000 today has not become eight times more valuable. It has become a larger number in a unit that has shrunk. Long term contracts, retirement plans, and business models built on fiat pricing are all quietly distorted by a unit of account that drifts. We compensate with inflation adjustments and cost of living clauses because we know, on some level, that the number cannot be trusted across time.

Three tests. Three failures.

What Would Actually Pass?

Imagine designing money from scratch. You would want it scarce by design, so that no issuer could dilute it overnight to fund a war or win an election. You would want it transferable without permission, so that no third party could freeze it, censor it, or exclude someone from using it. You would want it divisible to any denomination, so it could handle a coffee or a skyscraper with equal precision. You would want it durable across time, immune to physical decay. You would want it verifiable without trust, so that any party could confirm its authenticity without relying on an institution to vouch for it.

These are not radical requirements. They are the basic job description.

For most of human history no single thing satisfied all of them. Gold came closest but failed on transferability and divisibility at scale. Fiat currency solved the convenience problem but introduced an issuer with infinite supply and a track record of abuse.

Something now exists that satisfies every criterion on the list. It has no issuer. Its supply schedule is mathematical, not political. It is transferable across any border to any person without permission from any institution. It is divisible to eight decimal places. It has been running without interruption for seventeen years.

The market is in the early stages of figuring this out.

The Definition Always Mattered

Money is not what governments say it is. It is not what central banks print. It is not the number on your screen that shrinks a little every year while you are told prices are rising for other reasons.

Money is what passes the audit. A reliable store of value. A friction-free medium of exchange. A trustworthy unit of account.

We have been using a broken definition for so long we forgot there was a standard to measure against. The standard did not change. The money did.

— Waldo

The Cantillon Letter publishes weekly. If this made you think differently about something you use every day, share it with one person who would push back.